Map操作

1 | dict["w"] = "watermelon" |

Python两列表同位置同元素个数

a:[0, 0, 1, 0, 0, 0, 0, 0, 0, 1]

b:[1, 0, 1, 1, 0, 0, 0, 0, 0, 0]

map(cmp,a,b).count(0)

若是只判断“1” 的个数呢

map(lambda x,y:x+y, a, b).count(2)

或者sum(map(lambda x, y: 1 if x==y==1 else 0, a, b))

参考:https://uqer.io/community/share/54ca15f9f9f06c276f651a56

numpy

1 | import numpy as np |

布尔操作

由于Python中的布尔运算使用and、or和not等关键字,它们无法被重载,因此数组的布尔运算只能通过相应的ufunc函数进行。这些函数名都以“logical_”开头,np.logical_and np.logical_not np.logical_or np.logical_xor

1 | >>> a == b |

a = np.array([[1,2,3,4,5],[6,7,8,9,10]]) #原始数据

e = (a > 6) | (a <2) #构造对原始数据进行筛选的条件

a4 = np.where(e,a,0) #把满足条件的选择出来,原封不动的保存,不满足条件的元素置零

#本质上,就是把矩阵元素,按照条件分类.

a5 = a[e] #把满足条件的元素选择出来,构成新的元素子集合

1 |

|

x = np.arange(6).reshape(2,3)

x

array([[0, 1, 2],

[3, 4, 5]])

np.argwhere(x>1)

array([[0, 2],

[1, 0],

[1, 1],

[1, 2]])

1 |

|

s = Series(np.random.randn(5), index=[‘a’, ‘b’, ‘c’, ‘d’, ‘e’], name=’my_series’)

d = {‘a’: 0., ‘b’: 1, ‘c’: 2},s = Series(d)

Series(d, index=[‘b’, ‘c’, ‘d’, ‘a’]),Series(4., index=[‘a’, ‘b’, ‘c’, ‘d’, ‘e’])

serices 的选择和boolean过滤:

s[:2],s[[2,0,4]],s[[‘e’, ‘i’]]

s[s > 0.5]

‘e’ in s

1 | ## DataFrame的创建 |

df = DataFrame(columns=(‘lib’, ‘qty1’, ‘qty2’))或df = DataFrame(d, index=[‘r’, ‘d’, ‘a’], columns=[‘two’, ‘three’])

d = {‘one’: Series([1., 2., 3.], index=[‘a’, ‘b’, ‘c’]), ‘two’: Series([1., 2., 3., 4.], index=[‘a’, ‘b’, ‘c’, ‘d’])},df = DataFrame(d)

d = {‘one’: [1., 2., 3., 4.], ‘two’: [4., 3., 2., 1.]},df = DataFrame(d, index=[‘a’, ‘b’, ‘c’, ‘d’])

d= [{‘a’: 1.6, ‘b’: 2}, {‘a’: 3, ‘b’: 6, ‘c’: 9}],df = DataFrame(d)

1 | **行拼接**:for i in range(5):a = DataFrame([np.linspace(i, 5*i, 5)], index=[index[i]]),df = pd.concat([df, a], axis=0) |

print df.index

print df.values

1 | **DataFrame选择和切片**: |

print df[‘b’][2]

print df[‘b’][‘gamma’]

print df.iloc[1]

print df.loc[‘beta’]

print df[1:3]

bool_vec = [True, False, True, True, False]

print “Selecting by boolean vector:”

print df[bool_vec]

print df[[‘b’, ‘d’]].iloc[[1, 3]]

print df.iloc[[1, 3]][[‘b’, ‘d’]]

print df[[‘b’, ‘d’]].loc[[‘beta’, ‘delta’]]

print df.loc[[‘beta’, ‘delta’]][[‘b’, ‘d’]]

最快访问:at,iat

print df.iat[2, 3],print df.at[‘gamma’, ‘d’]

最快访问的智能化:ix

print df.ix[‘gamma’, 4],print df.ix[[‘delta’, ‘gamma’], [1, 4]],print df.ix[[1, 2], [‘b’, ‘e’]]

1 |

|

df = df.reindex(df.index|set([‘e’]))

df = df.reindex(list(df.index).append( [ ‘c’, ‘d’, ‘e’ ]))

pd.set_option(‘display.width’, 200)

dates = pd.date_range(‘20150101’, periods=5)

df = pd.DataFrame(np.random.randn(5, 4),index=dates,columns=list(‘ABCD’))

df2 = pd.DataFrame({ ‘A’ : 1., ‘B’: pd.Timestamp(‘20150214’), ‘C’: pd.Series(1.6,index=list(range(4)),dtype=’float64’), ‘D’ : np.array([4] * 4, dtype=’int64’), ‘E’ : ‘hello pandas!’ })

stock_list = [‘000001.XSHE’, ‘000002.XSHE’, ‘000568.XSHE’, ‘000625.XSHE’, ‘000768.XSHE’, ‘600028.XSHG’, ‘600030.XSHG’, ‘601111.XSHG’, ‘601390.XSHG’, ‘601998.XSHG’]

raw_data = DataAPI.MktEqudGet(secID=stock_list, beginDate=’20150101’, endDate=’20150131’, pandas=’1’)

df = raw_data[[‘secID’, ‘tradeDate’, ‘secShortName’, ‘openPrice’, ‘highestPrice’, ‘lowestPrice’, ‘closePrice’, ‘turnoverVol’]]

print df.shape

print df.head()

print df.tail(3)

print df.describe()

print df.sort(columns=’tradeDate’).head()

df = df.sort(columns=[‘tradeDate’, ‘secID’], ascending=[False, True])

print df[df.closePrice > df.closePrice.mean()].head()

print df[df[‘secID’].isin([‘601628.XSHG’, ‘000001.XSHE’, ‘600030.XSHG’])].head()

print df.dropna(subset=[‘closePrice’]).shape

print df.dropna(thresh=6).shape

print df.dropna(how=’all’).shape

print df.dropna().shape

print df.fillna(value=20150101).head()

print df[‘closePrice’].value_counts().head()

print df[[‘closePrice’]].apply(lambda x: (x - x.min()) / (x.max() - x.min())).head()

dat1 = df[[‘secID’, ‘tradeDate’, ‘closePrice’]].head()

dat2 = df[[‘secID’, ‘tradeDate’, ‘closePrice’]].iloc[2]

dat = dat1.append(dat2, ignore_index=True)

dat1 = df[[‘secID’, ‘tradeDate’, ‘closePrice’]]

dat2 = df[[‘secID’, ‘tradeDate’, ‘turnoverVol’]]

dat = dat1.merge(dat2, on=[‘secID’, ‘tradeDate’])

df_grp = df.groupby(‘secID’)

grp_mean = df_grp.mean()

df2 = df.sort(columns=[‘secID’, ‘tradeDate’], ascending=[True, False])

print df2.drop_duplicates(subset=’secID’)

print df2.drop_duplicates(subset=’secID’, take_last=True)

dat = df[df[‘secID’] == ‘600028.XSHG’].set_index(‘tradeDate’)[‘closePrice’]

dat.plot(title=”Close Price of SINOPEC (600028) during Jan, 2015”)

obj.combine_first(other) 方法的作用是使用 other 中的数据去填补 obj 中的 NA 值,就像打补丁。而且可以自动对齐。

marketIndex[field]=(marketIndex[field]+stock_prices[field]).combine_first(marketIndex[field])

1 | **多重索引** |

df1=pd.DataFrame(np.arange(12).reshape(4,3),index=[list(“AABB”),[1,2,1,2]],columns=[list(“XXY”),[10,11,10]])

df1.index=pd.MultiIndex.from_arrays([list(“AABB”),[3,4,3,4]],names=[“AB”,”num”])

df = df.set_index([‘class’,’id’])

1 |

|

df1.columns.names=[‘XY’,’sum’]

df1.index.names=[‘AB’,’num’]

df1.index=pd.MultiIndex.from_arrays([list(“AABB”),[3,4,3,4]],names=[“AB”,”num”])

df1.swaplevel(‘AB’,’num’)

1 | 查询 |

df.loc[(‘A’,slice(None)),:]

df2.loc[(‘语文’,slice(None)),:]

UnsortedIndexError: ‘MultiIndex Slicing requires the index to be fully lexsorted tuple len (2), lexsort depth (0)’

对index排序后切片选择index

df2 = df2.sort_index(level=’课程’)

df2.loc[(‘语文’,slice(None)),:]

获取相应内容

.get_level_values() Index level int/name: 获取对应级别的索引

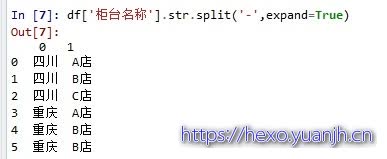

**列分裂**

## 参考

https://blog.csdn.net/weixin_38168620/article/details/80071141

https://blog.csdn.net/PIPIXIU/article/details/80232805

https://www.cnblogs.com/P--K/p/8672563.html

python入门系列

[python入门01廖雪峰python教程笔记](https://hexo.yuanjh.cn/hexo/4b73da9b/)

[python入门02简明python教程笔记](https://hexo.yuanjh.cn/hexo/7b7cd9f3/)

[python入门03int的四舍五入](https://hexo.yuanjh.cn/hexo/b16fcdae/)

[python入门04map,numpy,pandas速查](https://hexo.yuanjh.cn/hexo/ec7915af/)

[python入门05数据可视化](https://hexo.yuanjh.cn/hexo/9a29870f/)

[python入门06标准库实例教程学习笔记](https://hexo.yuanjh.cn/hexo/a698137d/)

[python入门07wtfbook疑问和验证](https://hexo.yuanjh.cn/hexo/b51782a2/)

[python入门08python\_interview\_question学习笔记](https://hexo.yuanjh.cn/hexo/a07a00a0/)